Charitable Giving through Donor Advised Funds

Introduction

Donor advised funds are a great way to manage charitable gifts. The basic idea is that you give money to the fund and get an immediate tax deduction. You choose how the money is invested, and it grows tax-free. At your leisure, you direct how the money is donated to charities. Fidelity, Schwab, and Vanguard all have very large donor advised funds (DAFs).

Charitable donations can only be deducted from your taxable income if you itemize deductions. In the wake of the Tax Cuts and Jobs Act of 2017, far fewer taxpayers are itemizing their deductions. The standard deduction got much bigger, so most taxpayers no longer itemize.

Standard Deduction vs Itemizing

In 2025, the standard deduction for an individual is $15,760, and for a couple it is $31,500. You will only want to itemize deductions if your deductions total more than the standard deduction. The largest deductions for most taxpayers are:

- State and local taxes (SALT)

- Home mortgage interest

- Charitable donations

The 2017 Act limited the SALT deduction to a maximum of $10,000. However, the “One Big Beautiful Bill” Act passed in July of 2025 increased it to a maximum of $40,000, phasing down to $10,000 beginning at modified adjusted gross income of $250,000 for single filers and $500,000 for joint filers.

That increase in the SALT deduction is likely to mean that many more people will want to consider itemizing their deductions.

Bunching Charitable Contributions

Many people may be able to save on taxes by “bunching” their deductions into a single year and itemizing in that year. The deduction most amenable to bunching is the one for charitable donations.

By making several years’ worth of charitable donations to a donor advised fund in a single year, you may be able to itemize in that year and then revert to taking the standard deduction after that.

An Example

To keep the math simple, let’s assume that in 2025 you expect your SALT, mortgage, and charitable deductions will be equal to your standard deduction. Let’s further assume that you are in the 22% tax bracket.

As it is, your SALT, mortgage, and charitable deductions are worth zero to you. That is, they do nothing to reduce your taxes. However, if you were to “bunch” your charitable contributions into 2025, every dollar that you give would reduce your taxes by $.22. Giving $10,000, for example, would reduce your taxes by $2,200.

You could certainly make direct charitable contributions to “bunch” your deductions in 2025. However, most of us like to make regular contributions, and most charities like to receive regular gifts. I know that is certainly true of most churches, which ask their members to make annual giving pledges in order to facilitate their planning and budgeting.

Giving to a donor advised fund makes bunching charitable donations easy.

Gifting Assets

If you have taxable assets that are worth more than their tax basis (cost), it will probably be more advantageous to donate the assets rather than cash. This is particularly true in the case of highly appreciated assets worth considerably more than their tax basis.

If you sell assets and donate the cash to the charity, you have to pay capital gains tax on the appreciation (current asset value – tax basis). However, if you donate the asset, you get to deduct the full current value, but you will owe no capital gains tax!

Some people have taxable assets for which they have no documentable tax basis. Even in the case of marketable securities, sometimes custodians haven’t kept good cost records, or never received cost records after an asset was transferred in from another financial institution. If you can’t document a tax basis, the IRS may require you to assume a tax basis of zero! In that case, you will owe capital gains tax on 100% of the asset value! Ouch! Giving the asset to charity solves the problem very nicely.

Donor advised funds (DAFs) make it easy to donate assets. Many DAFs (particularly the largest ones) even accept hard to value assets, such as real estate, private equity, and private debt.

A Suggestion for Sapient Clients

I have a specific suggestion for an asset donation for Sapient clients: highly appreciated shares of Vanguard Growth Index Fund ETF (VUG) held in taxable accounts. For some longstanding clients, VUG is currently trading at about twice its average tax cost. Assuming a long-term capital gains tax rate of 15%, that means that if you donate the entire position in VUG, you could save 7.5% of its current value in long-term capital gains taxes that you would otherwise have to pay.

However, you do not have to donate an entire position. Interactive Brokers (our custodian) allows you to donate specific tax lots. Optimally, you would want to donate those tax lots with the lowest tax cost and the most appreciation. That could mean that your tax savings would be even higher.

Unique Opportunity in 2025

2025 is likely to be an unusually attractive year in which to make “bunched” charitable donations. The reason is that starting in 2026, you will only be able to deduct the amount of your charitable contributions that exceeds 0.5% of your adjusted gross income (AGI). So, 2025 is that last year that you will be able to deduct the full amount of bunched charitable donations.

2025 is also the first year in which the higher SALT limitations will apply, making it more likely that itemizing your deductions will be attractive.

Selecting a DAF

When I started looking at donor advised funds (DAFs) I was surprised at how much they charge, both as a percentage of assets and as a flat annual fee. Fidelity, Schwab, and even Vanguard all charge an administrative fee of .60% per year on assets in their DAFs. On top of that are the expense ratios they charge in their investment funds.

Even the “no name” competitors, such as Charityvest and NPTrust charge about the same in annual fees. The one major exception is a firm called “Daffy.” (The “donor advised fund for you.”) It was co-founded by the former CEO of Wealthfront, which is a somewhat similar custodial product and platform.

Instead of asset-based fees, Daffy uses a simple, flat monthly membership fee. Daffy Membership Tiers and Fees are as follows:

- Supporter: Free for funds with a balance under $100.

- Contributor: $3 per month for individual or family funds with average annualized contributions up to $25,000.

- Family: $5 per month for a family fund with average annualized contributions up to $50,000.

- Benefactor: $20 per month for individual or family funds with the ability to make unlimited contributions and request custom investment portfolios.

Here are some comments from the news website Axios about Daffy:

“Daffy is challenging Vanguard on price, and by a huge margin. Someone with a $500,000 DAF would pay $236 at Daffy. Compared to $3,000 at Vanguard, $5,850 at Fidelity, or $7,100 at Schwab.”

“When Vanguard is 13X more expensive. Something very rare has just happened in financial markets: A startup called Daffy is challenging Vanguard Group on price. And by a huge margin.”

My Experience with Daffy

I just couldn’t bring myself to pay .60% in asset-based fees for the rather simple service of investing my money and periodically writing checks to various charities. I think it’s high time that a “disruptor” came along to shake up the market, and Daffy appears to be the one.

Be aware, however, that Daffy is a low-cost and highly automated operation. There is no customer service phone number. Everything is done either on their website (https://www.daffy.org) or on their phone app (if you have an Apple device—they do not support Android).

It is very easy to open an account. I will warn you, however, that if you choose to log in through Google or Facebook, you will never be able to switch to a password-based login. I thoughtlessly chose Google because it was easy, but now I regret that because I do not think it is as secure as using a password (with a password manager).

Rather than donate cash, I followed the advice I am giving you here and donated highly appreciated ETFs out of one of my taxable accounts at Interactive Brokers. I decided to donate 100% of several highly appreciated positions so that I wouldn’t have to deal with trying to donate specific tax lots.

The best way to do this is to start at the Daffy website first, giving the IB account information, ticker for each position, and number of shares. Rather than list a bunch of tickers and share amounts, the Daffy system only does one ticker and share combination at a time. The Daffy system will give you the specific DTC account information that you will need to put into the IB system.

In the IB system, after logging in, select “Transfer,” “Transfer Positions,” then “Outgoing.” Select Region as “United States,” then select “Free of Payment (FOP) Transfer of US Securities.” You will fill in the “Broker Information” you got from Daffy: “Apex Clearing Corporation (Part #: 0158)”, and the account number and name for your Daffy account. Do not “Save” the broker information because for some reason if you do that you can’t make a transfer at the same time. The IB form below lists all of the securities in your account and asks for the number of shares of each that you want to transfer.

In my case, the securities were transferred out the next day. So, what I did then was transfer in enough cash to repurchase the exact same tickers and shares in the IB account. That way, I put back into place the original portfolio that my models had determined was optimal.

You do not have to do anything to sell the securities you transfer into Daffy. They will be valued and your account credited with that value automatically. You no longer own those transferred positions. (I assume that Daffy immediately sells them.)

Once the securities are received at Daffy and your Daffy account is credited with their value, they appear to select a default investment portfolio for you based on the securities you transferred in. I assume that I was put in the “Standard – Growth Portfolio” probably because I transferred in several growth-oriented ETFs. However, you will probably want to select your own Daffy investment portfolio.

At the “Contributor” level ($3/month), you must select from Daffy’s “Pre-approved portfolios,” which heavily utilize low-cost Vanguard ETFs (just like we do at Sapient!). There are four categories of pre-approved portfolios:

- Conservative

- Cash

- Inflation-protected bonds

- Diversified bonds

- Standard

- Balanced (50/50 global stocks/bonds)

- Growth (75/25)

- Aggressive (90/10)

- Equities (100% US)

- ESG

- Crypto

I’m going to focus on the first two categories. Under “Conservative”, the “Cash” portfolio is an FDIC-insured bank account that only pays interest of .01%. “Inflation-protected bonds” is a 30/70 combination of VTIP and SCHP. I really like VTIP, but putting 70% into SCHP entails more interest rate risk than I prefer. The “Diversified bonds” portfolio is unusual for its heavy tilt towards credit risk and away from interest rate risk, and I like it a lot. It doesn’t have any stocks or TIPS bonds, which means it is more exposed to long-term inflation risk than may be ideal, but if you are going to give the money away fairly quickly anyway, this would be a good option, in my opinion.

Among the “Standard” pre-approved portfolios, all of them are combinations of four Vanguard funds:

These are the same four funds used in Vanguard’s LifeStrategy Portfolios that most of our clients use for benchmarks. The four portfolio options are very low cost and highly diversified. The two bond components are index exposures to the entire U.S. and international bond markets, so they have higher levels of interest rate risk than I prefer. Also, the Standard portfolios emphasize international stocks and bonds a bit more than most investors may prefer. For simple and easy solutions, I think that the “Standard” portfolios are all solid choices.

Another attractive feature of Daffy is that they are not an asset management company themselves. They allow you to create your own “Custom portfolio” by selecting from over 460 different ETFs in portfolios of up to 10 ETFs. I ended up deciding to create my own custom portfolio. It has been a few days, and I have not yet received back their approval of my little genius combination of ETFs. If you want a custom portfolio, you must bump up your membership level from “Contributor” at $3/month to “Benefactor” at $20/month. I may be kidding myself that my investment acumen can add at least $17/month in additional return, but we shall see.

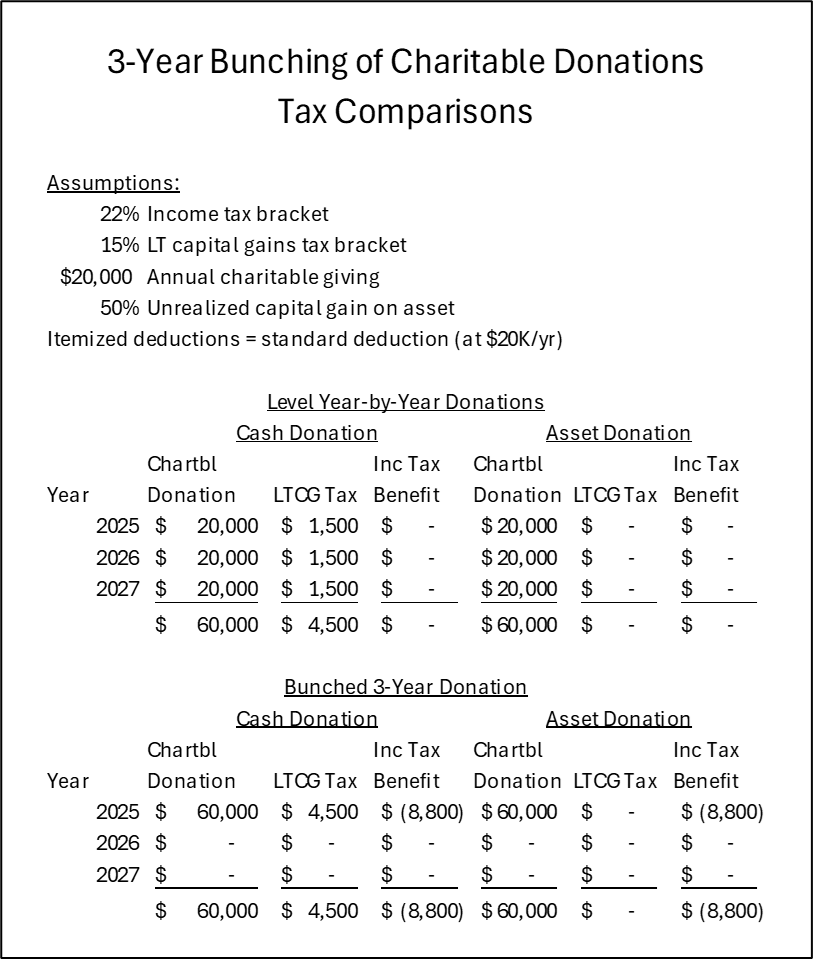

An Example

The table below provides a quick illustration of the various tax benefits available to you if you follow my advice and “bunch” your charitable contributions of the next three years in 2025 by making donations of highly appreciated securities from your taxable account.

Let’s assume that you have an asset in your taxable account that has appreciated to twice its original average tax cost. That means that if you sell the asset (which you would probably have to do at some point), you would pay long-term capital gains taxes (at 15% for taxable income below $533,400 single or $600,000 joint) on the unrealized gain of 50% of its value, or 7.5% of the asset value. ($1,500 LTCG on $10,000 unrealized gains commensurate with $20,000 total donations per year in the example below.) That’s a nice tax savings by itself, even if you don’t “bunch” your charitable donations.

Let’s further assume that the sum of your itemized deductions exactly equals your standard deduction, which includes charitable donations of $20,000 per year. If that is the case, you do not get any tax benefit from your charitable donations. However, if you bunch three years’ worth of charitable donations in the first year, then the value of the year 2 and year 3 donations you make in year 1 will be added to your itemized deductions in year 1. In the example below, that additional $40,000 in year 1 charitable deductions would reduce your income tax by $8,800 (assuming that you are in the 22% income tax bracket).

In total, your $60,000 charitable contribution could save you $4,500 in long-term capital gains taxes (15% of $30,000 in unrealized appreciation, or 7.5% of the total value contributed of $60,000) and $8,800 in income taxes (22% of the additional $40,000 in itemized charitable deductions, or 14.7% of the total value contributed of $60,000), for a total tax savings of $13,300, or 22.2% of your donation!

And that’s not even counting the fact that after 2025 you will lose the tax deductibility of charitable donations on the first .5% of your adjusted gross income, making “bunching” your future charitable donations in 2025 even more compelling!

Summary and Conclusions

- Donor advised funds (DAFs) give you an immediate tax deduction on amounts given.

- You can take your time deciding where and when to make your donations to individual charities.

- Most DAFs accept asset donations.

- Starting in 2025, the maximum SALT deduction increases to $40,000. That means more taxpayers will want to itemize deductions.

- DAFs make “bunching” charitable donations very easy.

- Donating appreciated assets is usually far better than donating cash from a tax standpoint.

- Sapient clients with taxable accounts may find that their position in Vanguard Growth Index Fund ETF (VUG) is a highly appreciated asset.

- Starting in 2026, you will only be able to deduct the amount of your charitable contributions that exceeds 0.5% of your adjusted gross income (AGI). So, 2025 is a great year for making bunched charitable donations.

- Nearly all donor advised funds (DAFs) charge an asset-based fee of .60%, on top of the expense ratios of the investments in their investment funds.

- A notable exception is a relatively new entrant, Daffy (“donor advised fund for you”). They charge a flat fee of only $3/month (or $20/month for larger levels of annual donations).

- I recently donated several highly appreciated ETF positions from a taxable Interactive Brokers account to a Daffy account, so I am able to help clients who would like to do the same.

- I then added enough cash to the taxable IB account to buy back the same number of shares of the donated ETF positions. I would suggest clients do the same.

- I would be glad to help clients select either a pre-approved portfolio or a custom portfolio at Daffy.