Which Risk Is More Important, Stock Risk or Bond Risk?

Nearly all portfolios are dominated by stock risk. For example, in a 60/40 stock/bond portfolio, stocks typically account for well over 90% of the risk. Therefore, in seeking to reduce overall portfolio risk, it is much more important to diversify stock risk than bond risk. Bonds currently have a low correlation with stocks, and so do a good job of diversifying stocks, but bonds also currently have low expected return.

Stocks are Much More Volatile Than Bonds

Stocks have always been much more volatile that bonds, as measured by the standard deviation of monthly returns. The graph below shows the history of the trailing 36-month standard deviation for both the S&P 500 and the Bloomberg Barclays US Aggregate Bond Index.

The current 36-month volatility of the S&P 500 is about 11%. Bond volatility is about 3%. It would be tempting to assume that stock risk contributes 11/14 (79%) of the total risk, and bonds 3/14 (21%). However, that is not how the math works. When comparing risks, the correct method is to use variances rather than standard deviations. (You may recall from your statistics class the saying “means and variances nicely add, but for standard deviations, adding is bad.”) Standard deviation is the square root of variance. The variance of stocks is about 121% and the variance of bonds is about 9%. Therefore, a good rough approximation of the risk contribution of stocks is 121/130 (93%), and for bonds 9/130 (7%). However, there is one more consideration, and that is the covariance between stocks and bonds. Here are the formulas:

Risk contribution of stocks = stock weight x stock variance + covariance of stocks with bonds

Risk contribution of bonds = bond weight x bond variance + covariance of stocks with bonds

Where,

Variance = standard deviation squared

Covariance of stocks with bonds = stock weight x stock std. dev. X bond weight x bond std. dev. X correlation between stocks and bonds

Stock and Bond Correlation Is Slightly Negative

The lower the correlation between stocks and bonds, the better job they do of diversifying each other and reducing portfolio risk. As shown in the graph above, the correlations were much higher in the 20th century. There seems to have been a regime shift in the 21st century, with notably lower correlations between stocks and bonds. Currently, the correlation is just below zero.

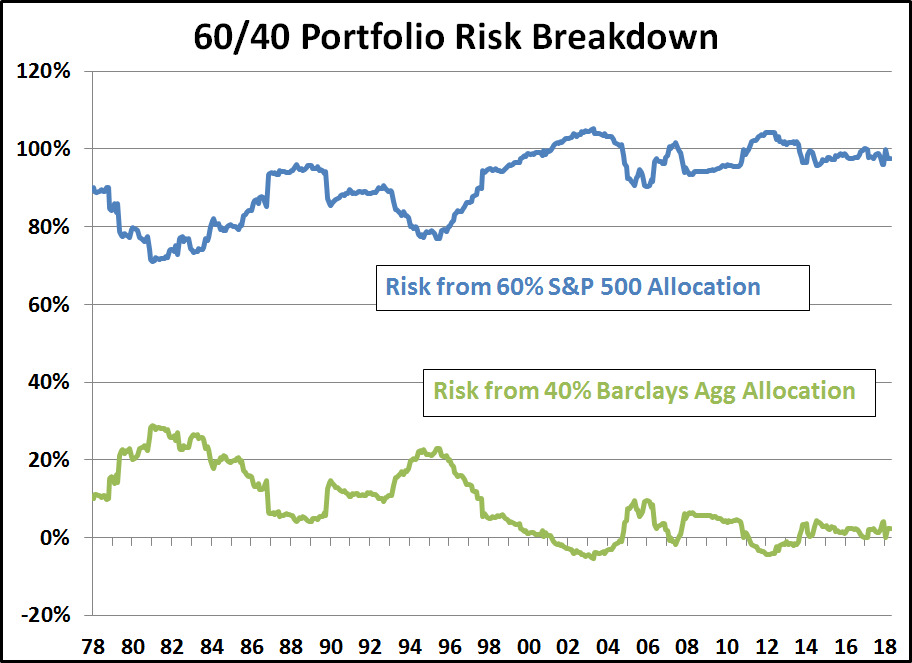

Stock Risk Contribution to a 60/40 Portfolio is Nearly 100%

When the correlation between stocks and bonds is negative, it is possible for stocks to contribute more than 100% of the risk of the 60/40 portfolio. Because of the prevalence of negative correlations between stocks and bonds in the 21st century, the average risk contribution from stocks has been 99%.

Bonds Currently Have a Low Expected Return

Bonds’ low correlation with stocks is very good news from a risk management standpoint. Bonds currently do a very good job of diversifying stock risk. The bad news is that bond yields are historically quite low. Therefore, expected returns from bonds are also quite low. If rates do revert back more toward historic norms, there will be capital losses as bond prices adjust. (Bond yields and bond prices move in opposite direction.) Recently, there has been some indication that the long-term reduction in interest rates may have run its course.

The current yield-to-maturity of the Bloomberg Barclays US Aggregate Bond Index is just under 3%. That’s not much better than the expected rate of inflation of around 2%. Also, the duration, or interest rate risk, of the Index is 5.8. That means that if interest rates increase by 1%, the expected price decline for the Index is -5.8%. That’s a lot of risk for not much return.

High Return Stock Diversification is Hard to Find

If reducing overall portfolio volatility is the objective, diversifying stock risk clearly should be the focus. Bonds have a correlation with stocks that is close to zero at present, a very attractive feature, but the expected return is only about 3%.

“Alternative investments” could potentially provide a solution, but their actual results have been largely disappointing. Most forms of alternatives investments involve a combination of illiquidity, high fees, opaque pricing, and difficult to understand strategies. These include hedge funds, private equity funds, and direct real estate investments. Alternative returns have largely been lackluster to say the least. Many varieties of “liquid alternative” mutual funds or ETFs have been offered, and these avoid many of the worst problems of traditional alternatives, but again, returns have been disappointing. In addition, the correlations of these supposed “alternative” investments with stock returns has been surprisingly high in many cases.

An attractive level of absolute return that is uncorrelated with stock returns would be ideal. More to come on this subject.